Whereas most individuals within the UK had been nonetheless in mattress within the early hours of Monday morning, the pound dived. It fell over 4% throughout Asia buying and selling to achieve its lowest ever stage in opposition to the greenback of US$1.035, whereas additionally hitting €1.079 in opposition to the euro. This was an distinctive fall, and continues its 3% decline in opposition to the US greenback on Friday in response to the hefty borrowing and tax-cutting in Chancellor Kwasi Kwarteng’s mini-budget.

Pound v US greenback since mini-budget

In parallel, merchants have been dumping British authorities bonds, which is driving up long-term rates of interest or yields. The yield on ten-year bonds, which closely influences mortgage charges and different financial institution lending, is now above 4% for the primary time since its highs following the 2007-09 monetary disaster.

UK Ten-year bond yields 2007-22

TradingView

The pound rebounded again above US$1.08 within the hours after the European markets opened, whereas ten-year bond yields have additionally eased just a little. It’s doable that the pound crash throughout the Asia session was over-extended as a result of buying and selling volumes within the British forex are decrease, which makes it simpler for smaller quantities of cash to make a much bigger impression available on the market. It’s not unusual for lows to be made in early Asia buying and selling, as has been the case in earlier forex crashes.

However, many analysts assume the pound reaching parity with the US greenback is more and more probably. So the place is all this heading and what’s going to the implications be?

The mini-budget gamble

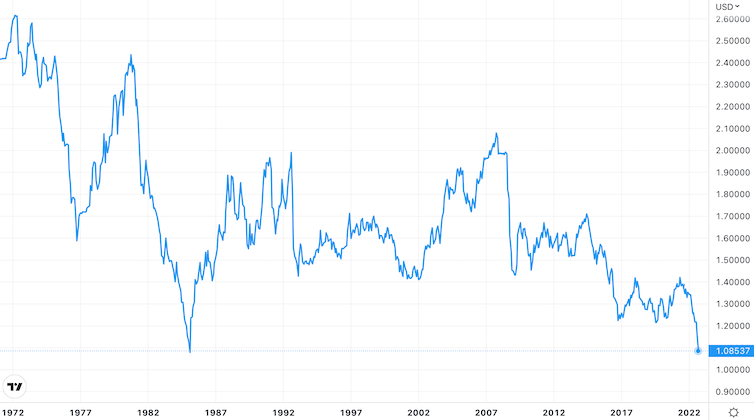

The pound has already been weakening for over a yr. That is partly as a result of the US greenback has been getting stronger because the US Federal Reserve has raised rates of interest and lowered the availability of {dollars} to try to get inflation below management, and partly as a result of the UK with its publicity to excessive gasoline costs and post-Brexit challenges doesn’t appear like an ideal prospect for financial development.

Pound v US greenback 1972-2022

TradingView

The brand new Truss authorities’s financial and financial insurance policies have made the market much more uneasy. They’re primarily based on a mix of power subsidies and big tax giveaways – notably to high-income households and householders – which can improve annual borrowing by greater than £100 billion.

The tax-cutting, which covers £45 billion of that improve, is a shift away from the direct transfers of cash from governments to households and companies which have been used to assist keep consumption since 2008 within the UK and lots of different nations. The advantages of tax-cutting in stimulating the financial system are extra delayed, which makes them extra unsure than direct handouts. In a state of affairs the place there’s arguably a necessity for instant motion to assist consumption as a result of individuals’s buying energy is being eroded by rising inflation, direct money transfers would have been quicker performing.

Tax cuts could not even work right here. Individuals within the UK could effectively see the destructive response from the markets and develop into extra pessimistic in regards to the prospects for the financial system. If that’s the case, they’re more likely to spend much less, which might weaken development versus growing it in the way in which that the federal government is hoping for. The federal government deficit – the hole between how a lot it spends in comparison with how a lot it brings in – would then improve and the tax cuts could be counterproductive.

Both method, the weaker pound goes to additional exacerbate UK inflation by making imports costlier. On the similar time, the rise in bond yields will doubtlessly injury development by growing lending prices and making shoppers really feel poorer. It should additionally make the additional authorities borrowing within the mini-budget much more costly than it was going to be already. All of that is more likely to put additional stress on the general public funds.

That is all a reminder that politically motivated financial coverage doesn’t sit effectively with the markets. With the federal government stimulating whereas the Financial institution of England is tightening financial coverage by elevating charges, they’re additionally performing as two opposing forces when it might be higher for them to coordinate with each other.

What a turnaround seems to be like

It’s however doable that the pound is now steadying amid hypothesis that the Financial institution of England could intervene with a charge rise to assist the forex. This might echo the Japanese central financial institution’s current intervention to assist the yen, which can also be in a historic decline in opposition to the US greenback.

But if the Financial institution of England does increase headline charges, presumably by 0.5 proportion factors or extra, this may have a detrimental impact on enterprise financing and financial exercise by additional growing the probability of upper charges on mortgages and enterprise loans. This may utterly negate the federal government’s makes an attempt to assist the financial system by slicing stamp responsibility and reversing the deliberate company tax hike – once more undermining the expansion plan.

The larger query is what occurs to US inflation. If it had been to fall because of a drop in the price of power imports and an improved international provide chain, the Federal Reserve could pivot on financial coverage. This might entail a pause on current interest-rate will increase and even the beginning of a reversal, which might take stress off currencies such because the pound and assist rescue the UK financial system.

Solely then would the supply-side measures within the mini-budget geared in direction of serving to companies with decrease company tax, less complicated planning and low-tax funding zones bear fruit. Even then, the federal government must hope that shopper and enterprise sentiment had not deteriorated an excessive amount of within the meantime. That every one quantities to an awfully dangerous gamble – if it doesn’t repay, count on extra hassle forward.

Jean-Philippe Serbera no recibe salario, ni ejerce labores de consultoría, ni posee acciones, ni recibe financiación de ninguna compañía u organización que pueda obtener beneficio de este artículo, y ha declarado carecer de vínculos relevantes más allá del cargo académico citado.